Several significant and recent changes to lending policy have stretched the ability of many foreign buyers to settle their active off-the-plan property purchases. They have also coincided with significant policy changes in China, our largest international investor in off-the-plan property. Taken together could they flatten our property market growth?

China has changed the rules for their citizens to get money out of the country. Previously property investors were able to get their ten percent deposit out, followed by another twenty per cent if required and then the some or all of the balance by settlement. Now we are being told they can get their ten per cent deposit out and probably another twenty per cent for settlement, all with considerable credit card gymnastics. So they are now reliant on borrowing in Australia.

The banks have recently tightened their lending criteria for foreign nationals. They reduced lending to 60% LVRs on valuation as the maximum loan.

The banks control valuation-for-finance as a risk reduction tool for them. The valuation is not a market appraisal. Instead they have very specific requirements for evidence of recent resales of comparable properties. Comparable resales are often difficult to achieve with off-the-plan apartment valuations in unique high rise city buildings.

If there is a shortfall in the valuation, or getting additional funds out of China where will the money come from? Is there a risk they may default and leave the developer holding unsold properties?

Additionally, Australian banks and other lenders have tightened their criteria on servicing for loans for foreign nationals. They have excluded income from self employed people and are questioning suspect paperwork.

Why have the banks done this and what are their concerns?

There is much discussion in the media about the percentage of off-the-plan property that is being sold to foreign nationals in the three eastern capital cities of Melbourne, Sydney and Brisbane.

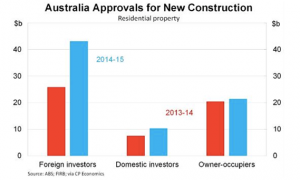

The graph below was reproduced from CP Economics in Robert Gottliebsen’s recent article in the Australian. Callan Pickering of CP Economics is a former Reserve Bank economist and an economic journalist. It shows FIRB and ABS data that about $75B was committed for purchases of off-the-plan property in the financial year 2015. This is broken down to about $43B or 57% from foreign investors. Domestic owner occupiers and investors made commitments to $33B or 43%.

The underlying facts are that foreign purchasing of property has increased three fold over the last five years. In 2010 it was 17% of sales and in 2015 it was 57%. In 2016, in response to these listed changes, Harry Triguboff of Meriton is indicating foreign national sales have dropped by 50%.

http://www.theaustralian.com.au/business/opinion/robert-gottliebsen/banks-exposed-to-looming-property-disaster/news-story/2924bce90be552d428b22bad9d6a2e91

As a result, it is very likely there will be multiple developments where foreign national clients won’t be able to borrow or self fund to complete their purchases. We have seen mass defaults like this before on the Gold Coast however this is likely to be much more wide spread over three large capital cities.

On the bright side, there is talk that superannuation has been ‘spoiled’ through recently proposed changes by both political parties. This is causing a shift to property as the investment of choice. The superannuation sector is worth about $2Tr with about 30% in SMSF. If we assumed ten per cent of SMSF funds were invested in property, both new and existing, it would be about $60B.

There is likely to be a mess with up to 53 per cent of purchasers affected. The banks have lent to developers and are not going to lend to their clients. How far will this spread? Do we threaten the export of education because families can’t buy property for their children to live in while they study? Do we threaten tourism as investors can’t complete their apartment purchases that they intended to visit frequently? Was lending to support speculation in Australian property by foreign nationals a smart move to begin with?